We help brands drive internal capability, operational and executional improvements to achieve excellence in brand, creative and e-commerce strategy execution. Providing services and solutions across strategy management, internal enablement, capability building and executional support provision.

Flagship clients

![]() (EMEA) 14 markets

(EMEA) 14 markets

![]() (EMEA) 47 markets

(EMEA) 47 markets

(EMEA) 17 markets

(EMEA) 17 markets

![]() (WHQ)

(WHQ)

Luxury depends on a fragile equilibrium between visibility and scarcity. Successful luxury brands have always told stories to bring in customers. And, these stories used exclusivity to make their customers feel part of an elite club. In fear of sacrificing that same sense of exclusivity, many luxury brands have been hesitant to branch out online. Many fear(ed) and believe(d) that internet's underlying democratisation power is at complete odds with exclusivity, scarcity and availability only to select few. As reported by The Economist back in 2010, Jean-Noel Kapferer, internationally acknowledged and cited by literature as one of the most influential experts in luxury brand management went as far as to claim that once an item is sold online, it ceases to be a luxury item. Some of these beliefs, as well as lack of practical know-how and capacities for digital transformation, made luxury retailers and luxury brands some of the slowest to embrace eCommerce as a distribution channel. And for a while, it looked like luxury goods and brands were not being touched by the eCommerce revolution. Today, however, even the strongest luxury holdouts have pivoted from their previous positions and not only do they see the value in selling to online consumers, but paradoxically, for foreseeable future place bets that the majority of luxury market growth will be coming from e-commerce. Luxury brands had a hard awakening to e-commerce opportunities.

Luxury brands' hard awakening to e-commerce opportunities.

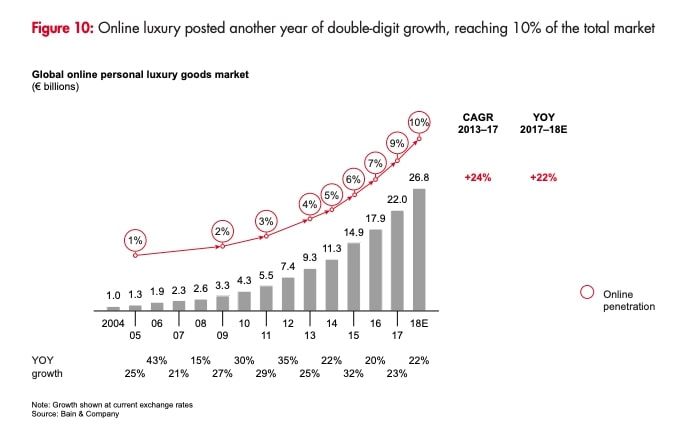

Within last few years, luxury brands aggressively turned to e‑commerce. The web’s share of global luxury sales ticked up to 9.0% in 2017 from 7.6% in 2016, and they were growing nearly five-times faster than total sales of prestige goods. That forced storied names in luxury to invest heavily in e-commerce and digital marketing. According to Bain & Company's "Luxury Goods Worldwide Market Study, Fall–Winter 2018" online luxury shopping continued to accelerate in 2018, growing 22% to nearly €27 billion; to represents 10% of all luxury sales. The Americas market made up 44% of online sales, but Asia is was emerging as a new growth engine for luxury online, slightly ahead of Europe.

Generations Y and Z accounted for 47% of luxury consumers in 2018 and for 33% of luxury purchase. More importantly they accounted for almost all the growth!

As Bain reports finds, generations Y and Z accounted for 47% of luxury consumers in 2018 and for 33% of luxury purchase. More importantly they accounted for almost all the growth! The reality is that Millennials comprise 13% of high net-worth households. And as a whole, they grew up shopping online. This means that they don’t have the same barriers to high-value online purchases that generations before them have. We’ve only scratched the surface of growth in this sector. According to the Bain & Company report, millennials and Generation Z shoppers accounted for about 85% of 2017’s growth in luxury goods sale.

Luxury brands can no longer deny the influence of younger consumers. Arguably, the greatest challenge luxury fashion brands now face is to decide how best to accommodate a younger, more diverse, tech-loving clientele. To answer this, they must understand not only how consumer expectations have changed but how the rapidly evolving luxury consumer’s wants and demands sit within this. “Consumers are clear that they see the future of luxury as digital” Deloitte highlights in their recent Global Powers of Luxury Goods research. The research finds that “the essence of luxury is changing from an emphasis on the physical (products) to a focus on the (digital) experiential.”

Arguably, the greatest challenge luxury fashion brands now face is to decide how best to accommodate a younger, more diverse, tech-loving clientele

Changing luxury consumers and their changing expectations

The rich are no longer ladies of leisure or housewives with infinite time to shop. The World Ultra Wealth Report of 2018 not only appointed that the group is getting younger and richer but more importantly: at least 65% of the world’s wealthiest families (Heads of Households) are first generation wealth, and depending on how you define the term “self-made” is over 80%. The proportion of the global ultra wealthy population whose fortunes are predominantly self-made continues to increase in 2017, while six of the ten richest people in the world have derived most of their wealth from the technology sector. Deloitte Global Powers of Luxury Goods 2019 report finds that a new consumer class has started to rise recently and is likely going to be very relevant in the future, especially for luxury brands: the HENRYs (High-Earners-Not–Rich-Yet).

Currently, they have a significant discretionary income and are highly likely to be wealthy in future. HENRYs are aged on average 43, with an income of more than US$100,000 and investable assets of less than US$1 million. HENRYs are digital savvy, love online shopping and are big spenders, in particular the Millennial HENRYs. To ensure future growth luxury brands must initiate and sustain longstanding relationships with this new consumer class who is likely to become or remain affluent or ultra-affluent in the future.

Global Powers of Luxury Goods 2019 | Bridging the gap between the old and the new

Despite the fact this insight was just recently acted on in practice of luxury retailers and brands, the tech-savviness characteristics of the luxury consumers was clearly reported on years ago. Back in September 2013, Google and Ipsos published a study entitled “How Affluent Luxury Buyers Buy Luxury Goods” that showed the importance of Internet in their purchasing decisions. The study makes clear that affluent luxury buyers are extremely tech savvy. As a matter of fact, every single luxury buyer surveyed was connected to the net somehow and used a smartphone, tablet or laptop. In average they have three connected devices and the Internet is their most used media (before TV, newspapers, radio or magazines). However, to act on these insights took leading luxury brands and retailers roughly 5 or more years.

The tech-savviness characteristics of the luxury consumers was clearly reported on years ago - as far as back in 2013

As luxury brands target very specific customer groups, they must build good relationships with each client and offer a superior purchasing experience.

Luxury e-commerce buying experience : no room for error. But...

Fact is that luxury doesn’t have any margin for error when it comes to e-commerce. Being initially conservative about whether to participate at all, they’re joining the e-commerce market at a time in which steps and rules have already been drafted on what shapes a satisfying shopping experience online. As Deloitte reports finds HENRYs are heavily influenced by modern technology, so are their expectations from an online buying experience. In an attempt to catch-up and translate the luxury shopping experience, which relies heavily in senses, into the Internet, luxury brands have tended to create websites that are too extravagant for their own good. Resulting in slow, not user friendly and chaotic spaces, difficult to navigate, that are far from the consumer expectations online.

Luxury brands are joining the e-commerce market at a time in which steps and rules have already been drafted on what shapes a satisfying shopping experience online as well as the average consumer expectations from it

How to recreate the luxury buying experience online has been a major discussion point and one of first hurdles to luxury e-commerce-as-a-channel adoption. Many brands didn’t have the digital expertise to replicate a white-glove experience online by themselves, so they partnered with multi-brand portals such as Yoox Net-A-Porter, MatchesFashion and Farfetch to run their online stores for them. With their digital savvy and understanding of the luxury market, these e-tailers know how to provide an “excellent” online shopping experience appropriate for a luxury brand, and they also have global reach.

Pre-purchase and post-purchase phase of the e-commerce buying experience

However, with couple of noteworthy exceptions, majority of investments and management focus has been on the pre-purchase and purchase phase of the buying experience, while post-purchase, has wrongly been downplayed. Augmented and virtual reality experiences, live streaming fashions shows, chatbots and web-chat shopping consultants stand contrasted with standard delivery service and standard carriers.

Majority of investments and management focus has been on the pre-purchase and purchase phase of the buying experience, while post-purchase has wrongly been downplayed

Customers who buy premium products online deserve a premium (post)purchase experience and service

Noteworthy exceptions to under-investments into post-purchase include Gucci's 2017 effort which launched a collaboration with online-only retailer Farfetch to provide 90-minute delivery in leading luxury regions. Net-a-Porter’s “You Try, We Wait” initiative calls upon personal shoppers to deliver orders to EIP (Extremely Important People) clients’ homes, wait until the pieces ordered have been tried on, and collect anything that needs to be returned. EIP customers account for 2 percent of Net-a-Porter’s customer base and generate 40% of sales.

Other brands have found success by providing unique post-purchase experience merging online and offline. Blome, a watchmaker founded in 1947, recently embraced digital commerce, and is now an official online reseller for 15 international luxury brands.

Benefits for customers include a dedicated staff of watchmakers and “masters,” rapid delivery of purchases, and free delivery and returns. Customers purchasing a watch worth more than €10,000 ($11,276) get special perks, as explained on its website: “Upon request, particular watches are proudly and personally explained, fitted and finally handed over to you by one of our watchmaker masters. Therefore, we like to invite you to spend a splendid shopping weekend on the Königsallee [in Düsseldorf], including an overnight stay in a suite at the Intercontinental Hotel. Your watch is celebratory given to you in our workshop. Alternatively, we gladly send watch and master to your home in Germany.” With such a formula, any absence of tangible luxury in the digital purchase process is more than overcome by the pleasure of the after-purchase experience—effectively reversing the sequence of events if consumers buy in a luxury brand’s physical store.

Any absence of tangible luxury in the digital purchase process is more than overcome by the pleasure of the after-purchase experience

China's JD.com is raising the bar for what consumers and brands will come to expect from a luxury e-commerce experience. JD Luxury Express, launched in 2017 for special deliveries of high-value luxury items sold on JD.com and its luxury goods platform, by popular demand was extended in 2018 to include sports, health, gifts and bags. The new service initially was launched in Beijing, Shanghai and Guangzhou, and as expected, expanded significantly over the next few years, making JD the first e-commerce company to roll out this type of luxury service on a large scale. White glove delivery is automatically included in the purchase of expensive, smaller items such as luxury watches and jewellery, which usually are delivered the same or next day in those cities.

A survey of JD customers showed 41.5% wanted luxury white glove delivery, especially when buying expensive products or purchasing gifts. Many customers who wanted the service said they would be willing to pay extra for it if their purchases didn’t automatically qualify, which is a finding that is confirmed in reports of both Bain & Company and Deloitte reports.

Need for elegance, however, does not end with the "Shop Now" button.

A luxury brand’s online presence should complement the traditional luxury consumer experience without replacing it. Brands must understand how they can provide a digital experience that will protect the value of the brand and provide consumers with the sophisticated elegance that defines luxury. Need for elegance, however, does not end with the "Shop Now" button. Luxury brands need to understand not only how consumer expectations have changed, but what are the rapidly evolving luxury consumer’s wants and needs from a total e-commerce buying experience - both pre-purchase and post-purchase.

Keeping up with the rapidly evolving expectations of affluent tech-savvy customers

The foundation of luxury has always been based on experiences. Luxury brands must acknowledge this and curate the digital e-commerce consumer journey touchpoints to create nuanced experiences that make the world of luxury tick. The core meaning of nuanced - to be done with extreme care to appreciate fine-point distinctions for which you have to be very detail-oriented to notice, needs to be infused into e-commerce pre-purchase, but more importantly the post-purchase experience. And this can only be achieved with deep consumer understanding and a cohesive, omni-channel strategy that spans technology, service, content and – critically - the implementation and operational expertise to sustain and grow the digital business.

With such rapidly evolving digital ecosystem, e-commerce market players and tech-savvy consumers, offering superior and exclusive experience both in pre-purchase and post-purchase becomes an elusive and ongoing challenge.

To satisfy luxury consumers’ expectations, a luxury brand must ensure its total e-commerce buying experience is superior. But, as hyper-servicing by omni-channels becomes more widespread, clients increasingly take its inclusion for granted, commoditising the consumer experience. In essence, with such rapidly evolving digital ecosystem, e-commerce market players and tech-savvy consumers, offering superior and exclusive experience both in pre-purchase and post-purchase becomes an elusive and ongoing challenge. Although the definition of luxury can be approached in different ways, all of them have gravitated towards six common characteristics : rarity, utility, price, craftsmanship, story, and perceived quality.

Generally, online consumers want greater convenience, cost-effective delivery and a quick and easy purchase process. Luxury consumers, however, are less hung up on the speed of delivery and instead expect a premium experience as standard – for which they are willing to pay. But how do you then craft an exclusive (post)purchase experience which will complement your brand's story, price point and perceived quality within a rapidly evolving e-commerce ecosystem where today's premium perk is tomorrow a simply a standard and expected service?

But how do you then craft an exclusive (post)purchase experience within a rapidly evolving e-commerce ecosystem where today's premium perk is tomorrow's standard and expected service?

First step would always be your specific brand identity and values, but second step would be the market level insights into the average consumer expectations from an e-commerce (post)purchase experience defined by the performance across phases of tracking, delivery, packaging & out-of-box experience, and returns and refunds - all which are shaped by the leading & key e-commerce players across markets. Luxury retailers need to understand that not only are they competing on experiences with other luxury brands, but when it comes to e-commerce, they're competing against all other e-commerce players which (luxury) consumers surely use and compare their experience. Can a free delivery from a luxury retailer be considered as an exclusive experience, when free delivery is standard with Amazon Prime which is available to about anybody and everybody?

Can a free delivery from a luxury retailer be considered as an exclusive experience, when free delivery is standard with Amazon Prime?

The length of delivery time, variety of delivery options, tracking visibility and communications, how your product is packaged, the ease of exchanges and returns—it all contributes to your brand perception (promises you make) as a whole.

Luxury Goods Worldwide Market Study, Fall–Winter 2018 by Bain & Company reports that 31% of online luxury sales take place through brand's own websites, thus the ability to craft and control the post-purchase experience is there.

Focusing on post-purchase to create exclusive experiences and drive e-commerce growth

Out of three phases (pre-purchase, purchase, and post-purchase) - the post-purchase phase carries most weight and is most influential in defining the total experience. So whether customers will choose to continue to shop with you or competitors depends mostly on post-purchase experience he has and had with your brand. Of course, an evaluation of the experience is always in comparison to your brand promises, but also relative to other retailers' performance in this segment. Namely, it is the collective performance of all retailers customers interact with within a single market that shapes implicit customer expectations and market performance averages.

Namely, it is the collective performance of all retailers customers interact with within a single market that shapes implicit customer expectations and market performance averages.

The post-purchase is an essential, yet often overlooked, stage of the eCommerce customer journey. Given that across the board repeat customers can account for up to 40% of store’s revenue, it’s important to have a strong post-purchase strategy in place in order to provoke repeat engagement, encourage referrals, and drive more revenue. Consumers have made it clear that brand experiences during the post-purchase phase have the greatest overall positive or negative impact on their brand relationship with retailers and their inclination to shop that retailer over competitors. And, so, it’s imperative that you remain ever aware of the fact that after you’ve thanked your customer for her order, you’re just beginning the most influential phase of his brand interaction with you. This is completely in-line with the "Peak-end" theory. The peak-end theory is a psychological rule in which an experience is evaluated and remembered based on the peak (most intense) point of the experience and/or the ending of the experience. It seems our recollection of events is impacted greatly by this interpretation of events experienced rather than the experience as a whole. Peak-end theory was created by the Nobel Prize-winning Israeli psychologist Daniel Kahneman. His definition is as follows:

The peak-end rule is a psychological heuristic in which people judge an experience largely based on how they felt at its peak (i.e. its most intense point) and at its end, rather than based on the total sum or average of every moment of the experience.

So, creating a truly exclusive and memorable post-purchase e-commerce experience starts with knowing the average market level end-experiences.

Companies need to both determine the implicit customer expectations from an online shopping experience and audit their own to know where they stand in contrast to the market averages and start defining and planning corrective actions. The research and insights into country by country implicit customer expectations from an online shopping experience with particular focus on the post-purchase experience is at the heart of the SO DIGITAL GLOBAL E-COMMERCE BRAND EXCELLENCE PLATFORM. It audits the most influential phase of customer brand relationship by contrasting the customer shopping experience across stages of delivery, tracking, packaging - out of box experience, returns & refunds ( the reality) versus brand set expectations (the promises).

It audits the most influential phase of customer brand relationship by contrasting the customer shopping experience across stages of delivery, tracking, packaging - out of box experience, returns & refunds ( the reality) versus brand set expectations (the promises). Our platform enables competitive cross industry performance benchmarking of best performing e-retailers across dimensions of online (post)purchase experience, including but not limited to, phases of delivery, tracking, packaging - out of box experience, and return & refunds.

To discover more how you can craft an exclusive post-purchase experiences for your e-commerce channel , contact us today for a free no-commitment 1-on-1 live walk through of our solution and client case of Nike (EMEA).

---------------------------------------------------------------------------------------------------------------

SO DIGITAL | GLOBAL BRAND EXCELLENCE SOLUTIONS is a technology company based in Amsterdam specialised in serving headquarters of global brands. We are proud partners of leading global digital growth brands like Nike (EMEA) and Uber (EMEA), but also other brands like TomTom (WHQ) and AS Monaco. With offices in Amsterdam, Berlin, Barcelona and Balkans we help global brands reduce complexity cost of global functional execution by delivering speed, scale and efficiency in strategy execution across markets.

References :

Fabien Bourrat, Mai Nilausen , "Luxury brands and e-commerce", Stockholm School of Economics, http://arc.hhs.se/download.aspx?MediumId=1425

Alba Romero Villa, "How to recreate the luxury buying experience online: e-commerce and luxury goods" https://www.slideshare.net/rvalba/alba-romero-villa-mba-in-luxury-business

Edge by Ascential. "As the luxury market moves online, is your brand ready?"

Don Davis, Internet Retailer, "Luxury brands aggressively turn to e‑commerce" https://www.digitalcommerce360.com/2018/10/23/luxury-brands-aggressively-turn-to-e%E2%80%91commerce/

Claudia D’Arpizio, Federica Levato, Filippo Prete, Elisa Del Fabbro and Joëlle de Montgolfi er, Bain & Company, "Luxury Goods Worldwide Market Study, Fall–Winter 2018". https://www.bain.com/contentassets/8df501b9f8d6442eba00040246c6b4f9/bain_digest__luxury_goods_worldwide_market_study_fall_winter_2018.pdf

Sarah Shannon, BoF - Business of Fashion : "Hard Luxury Awakening to E-Commerce Opportunity" https://www.businessoffashion.com/articles/news-analysis/hard-luxury-awakening-to-e-commerce-opportunity

"Why Luxury Brands Are Racing to Embrace E-commerce", Knowledge@Wharton, https://knowledge.wharton.upenn.edu/article/luxury-brands-racing-embrace-e-commerce/

Ultra Wealthy Analysis: The World Ultra Wealth Report 2018, https://www.wealthx.com/report/world-ultra-wealth-report-2018/

Global Powers of Luxury Goods 2019 | Bridging the gap between the old and the new, https://www2.deloitte.com/content/dam/Deloitte/ar/Documents/Consumer_and_Industrial_Products/Global-Powers-of-Luxury-Goods-abril-2019.pdf

"How Affluent Shoppers Buy Luxury Goods: A Global View", Think With Google, https://www.thinkwithgoogle.com/consumer-insights/affluent-shoppers-luxury-goods-global/

eMarketer Editors, eMarketeer, "In Europe, Affluent Millennials Are Changing How Luxury Brands Approach Marketing", https://www.emarketer.com/content/in-europe-affluent-millennials-are-changing-how-luxury-brands-approach-marketing-0

JD.com Launches White-Glove Delivery For Luxury Products https://jdcorporateblog.com/jd-com-launches-white-glove-delivery-service-for-high-end-and-specialty-products/

JD.com Expands Luxury White Glove Delivery Service https://jdcorporateblog.com/jd-com-expands-luxury-white-glove-delivery-service/

Florine Eppe Beauloye, Luxe Digital, "Why Luxury Brands Are Investing In Online Retail" https://luxe.digital/digital-luxury-reports/online-luxury-retail-transformation/

Karen Doll, PositivePsychology.com, "What is Peak-End Theory? A Psychologist Explains How Our Memory Fools Us" https://positivepsychology.com/what-is-peak-end-theory/